SHARON’S CORNER

With tax season in full swing, we are just a humming along. Enjoying business on a much smaller scale and being more hands-on with clients again has been the perfect solution to continue my health recovery and spend more time with family too.

It’s been a couple months since I posted a new blog however there are many in the works. Make sure you check out the latest and updated ones including some popular ones like Car Ownership: Business Or Personal?, Bookkeeping Made Easy, Top QBO Blunders, Understanding The Basics Of Tax, and more. Let me know your thoughts, comments and/or questions.

Please remember to update your records with our new mailing address.

PO Box 64553

RPO Como Lake

Coquitlam, BC V3J 7V7

Have a question? Email or call us. And remember to check out our blogs, checklists and social media pages for more information on all things small business, tax, accounting and the Tri-Cities community.

SMALL BUSINESS AIR QUALITY IMPROVEMENT TAX CREDIT: Could Your Business Benefit?

The December 14, 2021 Economic and Fiscal Update proposed a temporary refundable small businesses air quality improvement tax credit of 25% on eligible air quality improvement expenses incurred by small businesses to make ventilation and air filtration systems safer and healthier.

The credit will be available for qualifying expenditures between September 1, 2021 and December 31, 2022 related to the purchase or upgrade of mechanical heating, ventilation and air conditioning (HVAC) systems, and the purchase of standalone devices designed to filter air using high-efficiency particulate air (HEPA) filters, up to a maximum of $10,000 per location. There is also a $50,000 maximum claim to be shared among all affiliated entities. The $10,000 and $50,000 limits apply to expenditures over all years (since the beginning of the program) rather than to each particular taxation year.

Eligible Entity

Eligible Entity

The credit is available to qualifying corporations, partnerships and individuals other than trusts. A qualifying corporation is a Canadian-controlled private corporation (CCPC) that has (in combination with associated corporations) less than $15 million in taxable capital employed in Canada.

Qualifying Expenditures

To qualify, expenditures must be made for a qualifying location in Canada used by the entity in its ordinary commercial activities.

Claiming The Credit

Expenses incurred September 1 - December 31, 2021 are claimed in the entity’s first tax year that ends on or after January 1, 2022, while expenses incurred January 1 - December 31, 2022 are claimed in the tax year in which the expenditure was incurred.

The credits are taxable in the taxation year in which they are claimed.

ACTION ITEM: Maintain and provide us with any receipts for amounts expended that may benefit from this tax credit.

FALSIFIED EMPLOYMENT RECORDS: The Penalties Can Be Large

FALSIFIED EMPLOYMENT RECORDS: The Penalties Can Be Large

With numerous COVID-19 benefits being based on employment and remuneration levels, the federal government has likely become increasingly concerned with falsified employment records. However, this is not a new issue. In particular, the government already has experience dealing with false records used to increase access to employment insurance (EI) benefits.

Employers can face penalties of up to the greater of $12,000 and the total of all claimants’ penalties in relation to the offences. In addition, false claims by the applicant would result in an increased number of required hours to qualify for EI benefits in the future, with the specific number dependent on the value of the EI overpayment.

A September 14, 2021 Federal Court case addressed a $15,277 penalty that was assessed for a single employee’s records.

In respect of COVID-19 subsidies, employers may be subject to penalties including the following:

- loss of all CEWS, CERS and CRHP benefits for the period plus a 25% penalty for manipulations of revenue;

- loss of all CRHP benefits for the period plus a 25% penalty for manipulations of remuneration;

- gross negligence penalties of 50% of any applicable disallowed claims;

- third-party penalties to advisors equal to their compensation from the employer plus as much as $100,000 in situations of culpable conduct; and/or

- in the extreme, criminal liability for false statements, attracting penalties of up to 200% of the excessive claim and potential imprisonment for upwards of five years.

ACTION ITEM: Maintain supporting employment activity documentation as the government will be looking for situations in which employment records were falsified.

CORPORATE ADVERTISING & PROMOTION EXPENSES: CRA Increasing Reviews

CORPORATE ADVERTISING & PROMOTION EXPENSES: CRA Increasing Reviews

Over the past few years, CRA has taken a targeted approach in reviewing amounts claimed under specific lines (based on the type of claim) of a corporate tax return. Various projects conducted included reviews of professional fees, travel expenses and the purchase of certain vehicles.

CRA has recently focused their efforts on advertising and promotion expenses claimed by corporations. As part of this most recent project, CRA is asking for the following:

- a detailed list of the transactions (or the general ledger entries) related to the expenses; and

- a copy of the invoices and receipts for the ten largest transactions included in the expenses.

While there are many reasons to obtain this type of information, CRA may be analyzing whether any amounts deducted were personal, not wholly or partially deductible, or should have been capitalized. For example, provided no exceptions are available, amounts paid for food, beverages or entertainment are only 50% deductible to the corporation. Also, green fees for golf and membership fees in a golf club are not deductible regardless of whether they are incurred for business purposes.

ACTION ITEM: Be aware that additional CRA activity in these areas could result in extra time and administrative costs.

TEACHERS & EARLY CHILDHOOD EDUCATORS: Expanded Access To Tax Credit

TEACHERS & EARLY CHILDHOOD EDUCATORS: Expanded Access To Tax Credit

The eligible educator school supply tax credit is a refundable tax credit that allows teachers and early childhood educators to claim up to $1,000 for amounts expended (for which no allowance or reimbursement was provided) for supplies and some durable goods used to teach or facilitate students’ learning. Individuals must have a certificate from their employer attesting to the eligibility of their expenses for the year.

Shift To Online Learning

In an October 19, 2021 Technical Interpretation, CRA stated that if a shift has been made to an online classroom due to COVID-19, supplies consumed could still be eligible for the educator school supply tax credit.

Enhancements To The Credit

The government has proposed to enhance the eligible educator school supply tax credit to 25% of eligible supplies from the existing 15% credit and expand the list of durable goods eligible for the credit, both effective for 2021 tax years. The limit of $1,000 of eligible supplies remains unchanged.

The expanded list of durable goods includes all of the following (the first four items were previously allowed, while the other items have been added for 2021 and onwards):

- books;

- games and puzzles;

- containers (such as plastic boxes or banker boxes);

- educational support software;

- calculators (including graphing calculators);

- external data storage devices;

- web cams, microphones and headphones;

- multimedia projectors;

- wireless pointer devices;

- electronic educational toys;

- digital timers;

- speakers;

- video streaming devices;

- printers; and

- laptop, desktop and tablet computers, provided that none of these items are made available to the eligible educator by their employer for use outside of the classroom.

ACTION ITEM: Ensure to provide receipts for amounts expended by teachers and early childhood educators based on the expanded list of eligible expenses for the credit.

COVID-19 BUSINESS SUPPORTS: Targeted Measures

In the Fall of 2021, the government revised several business supports provided due to the COVID-19 pandemic.

The changes include extending the Canada Recovery Hiring Program (CRHP) to May 7, 2022 and increasing the subsidy rate to 50%. The wage and rent subsidies under the previous Canada Emergency Wage Subsidy (CEWS) and the Canada Emergency Rent Subsidy (CERS) are also being modified to provide much more targeted support to assist the hardest-hit businesses and those in the tourism and hospitality sector and extended to May 7, 2022.

While the base rules for the wage and rent subsidies under the more targeted approach are similar to the previous CEWS and CERS rules, there are some changes.

Both the wage subsidy and the rent subsidy are available under any of the following three gateways:

- Hardest-Hit Business Recovery Program – available to entities with a prior year revenue decline and a current period revenue decline of at least 50%;

- Tourism and Hospitality Recovery Program – available to qualifying tourism or hospitality entities with a prior year revenue decline and a current period revenue decline of at least 40%; and

- Local Lockdown Program – available for businesses in all sectors, subject to a qualifying public health restriction, with a current revenue decline of at least 40% (25% in some periods).

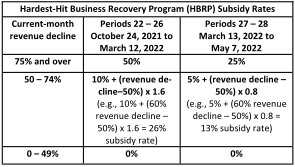

Hardest-Hit Business Recovery Program (HBRP)

Eligibility for the HBRP would require revenue declines of at least 50% for both of the following:

- the current month (determined under the existing CEWS and CERS rules); and

- the average of the first 13 CEWS periods (March 15, 2020 to March 13, 2021), referred to as the 12-month revenue decline.

The 12-month revenue decline would be calculated as the average of all revenue decline percentages from March 2020 to February 2021 (claim periods 1-13, excluding either claim period 10 or 11, which used the same comparative periods). Any periods in which an entity was not carrying on its ordinary operations for reasons other than a public health restriction (for example, because it is a seasonal business) would be excluded from this calculation.

The 12-month revenue decline would be calculated as the average of all revenue decline percentages from March 2020 to February 2021 (claim periods 1-13, excluding either claim period 10 or 11, which used the same comparative periods). Any periods in which an entity was not carrying on its ordinary operations for reasons other than a public health restriction (for example, because it is a seasonal business) would be excluded from this calculation.

The HBRP would be based on the qualifying remuneration (the same amounts previously eligible for CEWS) and qualifying rent expense (the same amounts previously eligible for CERS) at a rate based on the current-month revenue decline. At the minimum revenue decline of 50%, the subsidy would be 10%, rising to a maximum of 50% where the revenue decline is 75% or more. These subsidy rates would be halved for periods after March 12, 2022.

Lockdown support would also be available as under the previous CERS rules.

Lockdown support would also be available as under the previous CERS rules.

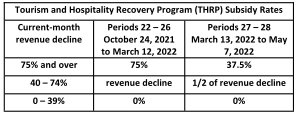

Tourism and Hospitality Recovery Program (THRP)

The THRP would target the tourism and hospitality sector, with examples including hotels, restaurants, bars, festivals, travel agencies, tour operators, convention centres, providers of cultural activities and convention and trade show organizers.

Eligibility for the THRP would require revenue declines of at least 40% for both of the following:

- the current month (determined under the existing CEWS and CERS rules); and

- the average of the first 13 CEWS periods (March 15, 2020 to March 13, 2021), referred to as the 12-month revenue decline (calculated in the same way as the HBRP).

At the minimum revenue decline of 40%, the subsidy would be 40%, equal to the revenue decline, rising to a maximum of 75% where the revenue decline is 75% or more. These subsidy rates would be halved for periods after March 12, 2022.

Lockdown support would also be available as under the previous CERS rules.

Increased Cap On Qualified Rent Expense

Under CERS, qualified rent expenses were limited to $75,000 per location and an aggregate of $300,000 for all locations within an affiliated group. The aggregate monthly cap is increased from $300,000 to $1,000,000 for rent subsidies under the new gateway.

Local Lockdown Program

Organizations that are subject to a public health restriction are proposed to be eligible for support at the same rates applicable for the THRP (see above), regardless of sector.

The base rules require having one or more locations subject to a public health restriction lasting for at least seven days in the current claim period that requires them to cease activities that accounted for at least 25% of total revenues during the prior reference period. This would not require meeting the 12-month revenue decline, only a current-month decline. It would be available to all affected organizations, regardless of sector.

Special rules were introduced to provide expanded access to this program from December 19, 2021 to February 12, 2022. The expansion allows entities to qualify if they are subject to a capacity-limiting public health restriction of 50% or more. In addition, the current-month revenue decline threshold is reduced to 25% (from 40%).

ACTION ITEM: Targeted wage and rent subsidies are still available to those particularly hard-hit entities or those in the tourism and hospitability industry. Ensure to apply if eligible.

Canada Worker Lockdown Benefit (CWLB): Modified Support For Individuals

The CWLB provides a $300 per week benefit to employees and self-employed persons unable to work due to a public health restriction lasting at least seven consecutive days. It will apply only to regions designated by the federal government as eligible in the period. This would be in regions where provincial or territorial governments have introduced capacity-limiting restrictions of 50% or more. CRA posted a webpage listing designated regions. As of January 11, 2022, Saskatchewan was the only region with no eligibility. Quebec and Northwest Territories had certain regions eligible, while all the remaining provinces and territories had all regions eligible for at least some periods.

To be eligible, the applicant must also meet the following criteria:

- SIN – have a valid social insurance number;

- Age – be at least 15 years of age on the first day of the week;

- Residency – be resident and present in Canada during the week;

- Tax return filed – have filed a 2020 income tax return

- Prior earnings – have had, for 2020, or in the 12 months preceding the day on which they make the application, a total income of at least $5,000 from employment, self-employment, parental benefits, Canada Emergency Response Benefits (CERB), Canada Recovery Benefits (CRB) or income prescribed by legislation. For 2022 claims, the additional option of using 2021 income will be available;

- Current benefits – no benefits are available for the same period with respect to EI, provincial parental benefits, the Canada recovery caregiving benefit or the Canada recovery sickness benefit; and

- Loss of income – the individual must either have:

- lost their employment during the lockdown period and been unemployed during the week;

- been unable to perform the self-employment activities they normally performed immediately before the lockdown period; or

- their average weekly income declined by at least 50% compared to their total average weekly employment and self-employment income for 2020 or the 12 months preceding the application (for 2022 claims, the additional option of using average weekly income for 2021 will be available).

Applicants who have voluntarily ceased to work, unless the cessation was reasonable, or failed to return to work when possible and reasonable to do so, are ineligible. Similar to the Canada Recovery Benefit, individuals will be ineligible for benefits during mandatory quarantine or self-isolation following a return from international travel. Where the inability to work results from a refusal to comply with a requirement to be vaccinated against COVID-19, the individual will be ineligible.

Where an individual received CWLB in 2021, their benefits will be reversed if they do not file their 2021 income tax return by December 31, 2022. Similarly, an individual receiving CWLB benefits in 2022 will lose entitlement if they do not file their 2021 and 2022 income tax returns by December 31, 2023.

Applications for benefits must be filed by the later of February 16, 2022, or 60 days from the end of the claim week.

ACTION ITEM: If you are eligible, ensure to make a timely claim. Also, if eligible, ensure your 2020 personal tax return was filed, and your 2021 return is also filed to avoid required repayments.

OLD AGE SECURITY (OAS): Clawback Planning

OLD AGE SECURITY (OAS): Clawback Planning

Individuals who normally receive OAS are occasionally surprised when some OAS is subject to a special tax (commonly referred to as a “clawback”) with their T1 tax filings due to high earnings. In particular, OAS is clawed back at a rate of 15% of adjusted income (AI) received in that year over an indexed threshold amount.

The current and upcoming threshold amounts are $79,845 (2021) and $81,761 (2022). If receiving maximum OAS in 2021 (assuming no changes for items like deferred application, being over age 75, etc.), the full amount will be clawed back if 2021 AI is $129,757 or higher.

AI is net income before the deduction of any clawback with a few modifications, such as removal of Registered Disability Savings Plan (RDSP) income inclusions.

OAS payments starting in July are subject to withholdings based on AI of the prior calendar year. If it is known that AI for the current year will be less than that of the prior year, Form T1213(OAS) can be filed to request reduced withholdings.

Some Planning Considerations

Defer Commencement Of OAS Receipt

Future OAS payment increases of .6% per month of delay (to a maximum of 36% for 5 years of deferral) are provided to compensate for the deferral of OAS pension payments. This flexibility may permit a person to reduce or eliminate the OAS clawback by deferring the receipt of OAS until the income of the person is below the AI clawback threshold. If OAS will be clawed back in its entirety, it costs noting to delay but provides the benefit of increased future payments. Increased OAS payments also increase the AI level at which all OAS is clawed back.

A further possibility for a high-income individual is to retroactively apply early in a year after reaching age 65 to receive up to additional 11 months of benefits in a single calendar year, hopefully retaining some benefits in that one year. For high-income seniors, application could be delayed resulting in the full 36% enhancement and 23 payments received in the year the individual reaches age 72.

Use Resources That Reduce AI

It is important to know how certain sources of income affect AI as any changes between the beginning clawback threshold and the amount at which OAS is completely eroded carry a 15% impact on OAS entitlement. Note that 115% of ineligible dividends and 138% of eligible dividends are included in AI. On the other hand, only 50% of capital gains are included.

Watch Out For Deductions

Certain deductions such as non-capital and net capital losses, the capital gains deduction, and the northern residence deduction will not reduce clawback. As such, for example, while no tax may need to be paid on the sale of qualified small business shares or qualified farm property, OAS could still be significantly impacted. On the other hand, deductions for pension splitting, which are discretionary, do reduce AI.

From an overall perspective, it may even be beneficial to shift pension income to the higher-earning spouse if it reduces clawback for the lower earner, despite the increase in marginal tax rates.

Time Income Inclusions

If an individual’s AI will unavoidably already fully eliminate OAS, consider whether additional amounts that have high impacts on AI could be taken into income in the current year, with the after-tax amounts to be used to fund needs in future years. Likewise, if far below the prescribed threshold, the same may be considered as additional amounts do not erode OAS until that threshold is reached. Of course, the advantages would have to be balanced against any differences in applicable marginal tax rates and other income-tested benefits.

Individuals should also consider whether funds needed for the year could be obtained from sources that do not impact AI at all, such as capital dividends, capital withdrawals from investments, trust distributions of capital, TFSA withdrawals, repayment of shareholder loans or obtaining new loans.

ACTION ITEM: Care should be taken to minimize the current year and future year clawbacks to Old Age Security payments.

TAX TICKLERS

- The annual TFSA limit for 2022 remains at $6,000. As such, if an individual has never contributed and has built room since the program’s inception in 2009, up to $81,500 can be contributed.

- Employees working from home in 2021 due to the COVID-19 pandemic will again have the option to claim a deduction against their employment income using the temporary flat rate method. The maximum claim will increase to $500 from $400 in 2020.

- Did you know? About 30% of first-time homebuyers received financial help from family members. The average amount gifted was $82,000 but as high as $130,000 and $180,000 in Toronto and Vancouver. These informal agreements should be documented in writing to protect all parties, especially to clarify whether the funds are a gift, a loan (and repayment terms) or an equity investment in the property.

- The federal climate action incentive (Alberta, Manitoba, Ontario and Saskatchewan) will convert from a tax credit claimed on personal tax returns to quarterly payments in 2022. The first payment will be made in July 2022 and will be a double payment for the first two quarters of 2022. Subsequent payments will be made each January, April, July and October.

**This publication is a high-level summary of the most recent tax developments applicable to business owners, investors, and high net worth individuals. This information is for educational purposes only. As it is impossible to include all situations, circumstances and exceptions in a newsletter such as this, a further review should be done by a qualified professional. No individual or organization involved in either the preparation or distribution of this letter accepts any contractual, tortious, or any other form of liability for its contents. For any questions… give us a call.